How to make money in a dislocation

Warren Buffet's USD 269 billion clue

Looking at analysis from Ray Dalio and considering Berkshire Hathaway’s significant move into cash it appears that soon-ish there may be large movements in indices, inflation and bonds. In fact that process appears to have started and current choppiness may extend into significant movements. Those well positioned for those movements will likely make significant gains, those who are under-prepared will suffer material losses.

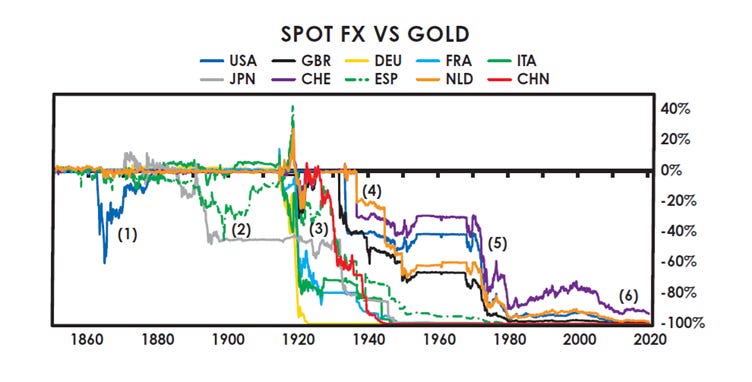

The chart from The Changing World Order illustrates how much gold one nominal unit of currency will buy over time – so if in 1900 that is 1.00 ounce, by 2020 that becomes 0.01 ounces (99% decline). To be fair, it is not surprising that inflation eats away at purchasing power over long periods – the key question is what assets will protect against and even outperform above inflation under different scenarios and to remain agile during the coming dislocation.

The best way to understand what’s coming next is to listen very carefully to the world’s most successful investors. In the last note, I covered the likely cycle that Ray Dalio could see with excess debts, excess deficits, money printing, increasing wealth inequalities and internal conflict. Looking at this wasn’t a theoretical exercise; it was designed to identify the likely scenario to prepare for by moving assets into categories that will survive and even thrive under that scenario. Sitting on the sidelines in cash will likely lead to very significant real (inflation adjusted) losses.

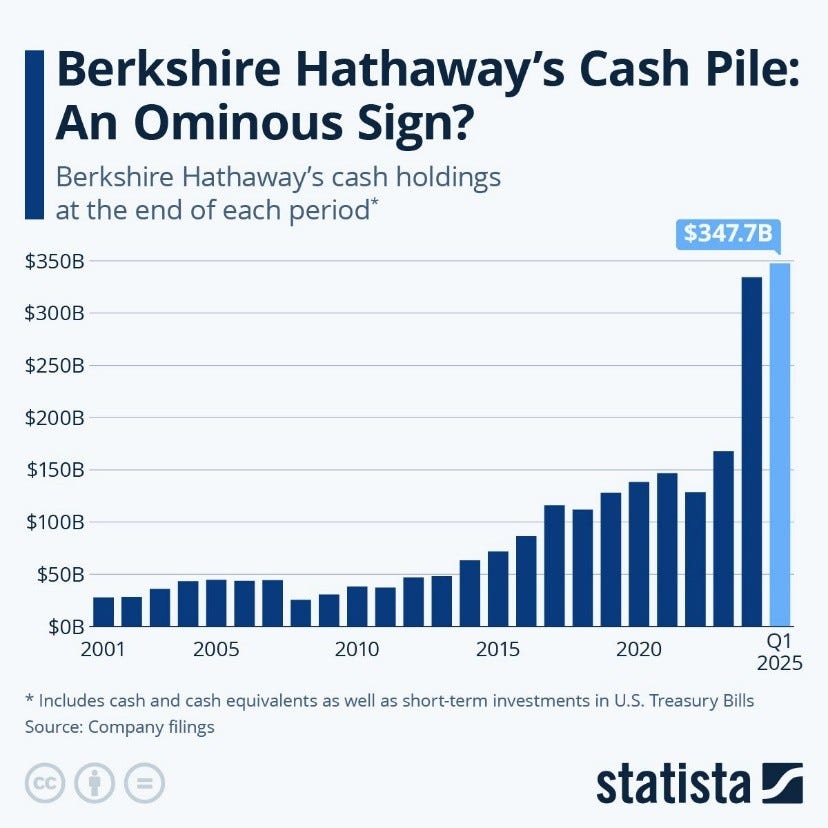

This note expands on the analysis from Dalio’s The Changing World Order and looks at the signal contained in Berkshire Hathaway’s huge cash pile of USD 369 billion. This is not an accounting investigation, but an attempt to gain real insights about how to position oneself for a dislocation.

These notes will provide some analysis with more specific insights reserved for paid subscribers. Finally for those who really want to prepare seriously, that can be done via 1:1 discussions on a fee paying basis (contact: info@thinkingcoalition.org). The classic 60:40 equity, debt portfolio is already broken and would perform horribly in an inflationary environment. Physical gold is an excellent hedge but forgoing possibly high returns post a correction is short sighted, Berkshire Hathaway cleaned up in 2008 by being the only bid.

Overview

As Warren Buffet handed over the reins of Berkshire Hathaway to new CEO Gregory Able, he dropped a pretty massive clue that Berkshire Hathaway expects parts of the U.S. market to do poorly from these price levels. At 31st December 2025 Berkshire Hathaway had a pile of USD 369 billion in cash and T-bills. Berkshire Hathaway dramatically increased its cash pile at the end of 2024 (see chart below to Q1-2025) and as at 31st December 2025 this had further increased.

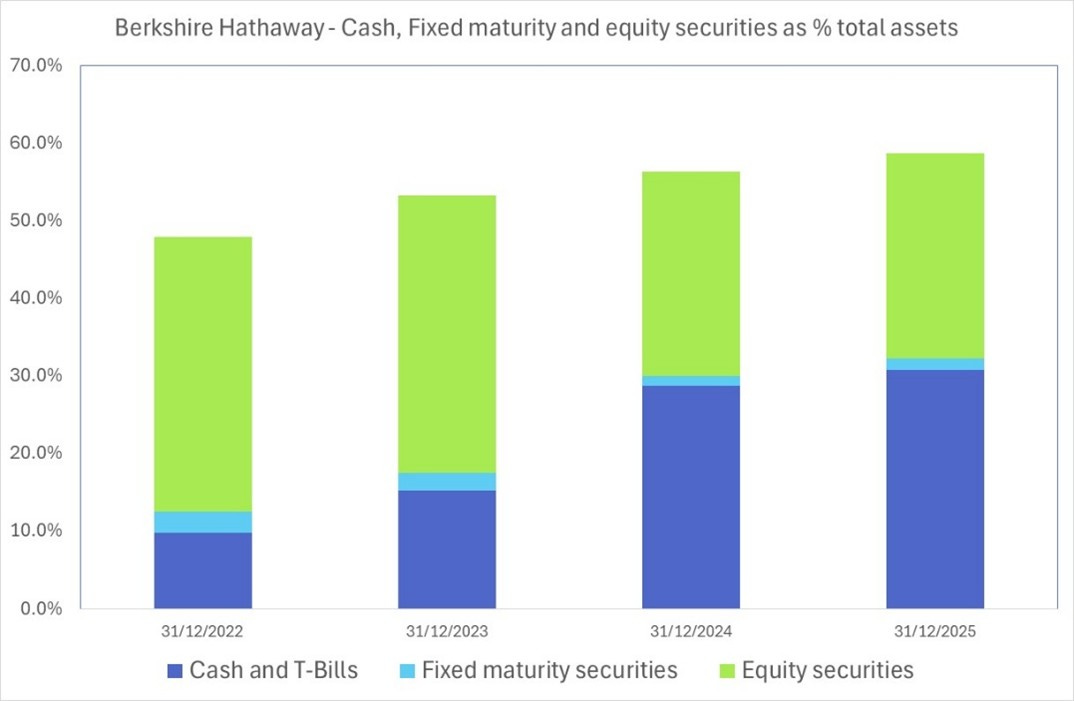

Berkshire itself has grown tremendously since 2001 (it now has assets of USD 1.2 trillion) so it makes sense to look at cash and T-bills as a percentage of total assets. The current position - just over 30% of total assets is way, way above its long run level of around 11%. Their equity investments (including equity method investments in companies in which Berkshire owns more than 20%, Heinz and Occidental) have correspondingly shrunk from 35.5% at the end of 2022 to 26.4% at the end of 2025.

You can make some inferences from this unusually large cash holding:

i) Berkshire believes that the assets it is selling are fully valued and will not offer decent returns going forward.

ii) The decision to hold cash implies that there are no other acceptable assets currently available that will generate a decent return (i.e. a low enough entry price level).

iii) Holding rather than returning the cash to shareholders implies that they expect that prices will fall and investment opportunities will materialise.

Simple maths suggests that if your aim is out-perform the S&P 500, with 30% of your assets in cash you are expecting a large fall. In a market in which the S&P 500 was rising, it would become very difficult for 70% of the portfolio to compensate for the fact that 30% was “doing nothing”. On the other hand if the S&P 500 index was falling, the 30% in cash doing nothing would itself generate outperformance.

This cash holding is particularly significant given Berkshire Hathaway’s record of stellar performance investing in corporate America – achieving a cool 6,099,294 % (yes that’s six million, ninety-nine thousand and two hundred and four per cent) over the period from 1964 to 2025. This is equivalent to an annually compounded rate of 19.7% compared to 10.5%. for the S&P 500 with dividends included. The annual report correctly describes Warren Buffet as “arguably the greatest investor of all time.”

The site Hedgefollow.com provides an overview of the big sales which include Apple, Bank America Corp and Verisign, suggesting that going forward returns will be poor in these stocks. Apple with an acquisition cost of USD 27.30 per share was up almost ten times by the end of 2025. This is classic Buffet in that i) he had the foresight to buy and ii) the balls to buy in volume and iii) the patience to hold on 10 years and counting for the remaining holding.

Buffet’s Japan diversification

Another interesting feature of Buffet’s investments is his diversification into Japan. Given the phenomenal success that he has enjoyed in the U.S. (with a 19.7% annual compounded return) one imagines that Buffet feels that he can do just as well in Japan.

So far that decision has worked out like a charm. His Japan position across five conglomerates (USD 35.4 billion at market) is up 130% over cost. You can do some back-calculation to work out when he bought Mitsubishi (for example) – this works out at an average cost price equivalent to the level in April 2023. He has made 243% over cost over roughly 3 years, equivalent to a 51% rate of return compounded.

Suggestions for positioning in 2026

In the last article, I spent some time explaining how Ray Dalio views possible scenarios for the U.S. given the ways in which previous empires have expanded and contracted over history. The plausible base case scenario that we have is untenable debt levels, followed by zero rates and money printing and then high inflation to inflate those debts away. Of course multiple other scenarios are possible and have some probability associated with them, including a 1930s style deflationary bust or simple “business as usual” with a building debt pile and moderate inflation for years.

But how to position in the base case?

(continued for paid subscribers)

Continue reading this post for free, courtesy of Thinking Coalition.

| A guest post by

|