How to create £ 900 billion

Possibly the most important paper on money you will ever read

Today I will start with a question: what were the worst financial costs of lockdown? Worst in terms of the amount spent and the futility or fraudulence of its alleged purpose?

Did you think about burning piles of useless PPE equipment?

Few people, I suspect, would have pointed to the estimated £ 150 billion bill (OBR higher rate scenario1) that “We The People” have been left with for the privilege of having our money devalued through mass money creation.

Before I get into the nitty gritty of that figure, I will firstly explain how new money is created. Fear not, the truth is far simpler than you have been led to believe. In fact, not only is the truth buried under a mountain of obfuscatory jargon, but also the theory of banking is mistaught!

This bombshell observation was dropped by none other than the Bank of England (BoE) itself in a note which states that “the relationship between reserves and loans typically operates in the reverse way to that described in some economic textbooks2”. In fact this is an understatement and should read ALL economic textbooks. As an aside, we have to ask whether the authors of economic textbooks (particularly the classic Economics by Begg, Fischer and Dornbusch) were just plain dumb? Given that they were all highly respected economists we can answer with a firm “no.” In my view, the theory of banking was deliberately mistaught.

The fairytale version of banking that I and many others were taught outlines how Mr. Jones spends some of his salary and takes the remainder and deposits it in his account with the local bank. The bank then lends those funds on to Business Z. Business Z expands and also makes a profit and pays interest to the bank. The bank retains some of the interest and passes the balance to Mr. Jones in the form of deposit interest. Everyone lives happily ever after.

I never really liked that version because it implied that there would be some kind of link between wages (and corporate cash flows), savings (household and corporate) and loans, whereas no such link exists in reality. As I covered in a recent note, debt has ballooned relative to GDP and now stands at 250% of GDP in the US (household, corporate and government combined). The equivalent figure is 219% for the UK according to the Bank for International Settlements (BIS).

In fact, the BoE dropped a big clue in their paper confirming that deposit creation actually worked in the way I had long suspected where deposits are generally created from loans. For bookkeepers this is a simple debit and credit entry, when the bank signs a loan agreement it creates an asset with the simultaneous liability being the deposit account of the borrower into which the loan proceeds are credited. The BoE paper is very clear on this “fountain pen money, created at the stroke of bankers’ pens when they approve loans.” This reality helps to explain how it is possible that loans (and deposits) in an economy can increase by so much more that economic activity as measured by GDP.

“When a bank makes a loan to one of its customers it simply credits the customer’s account with a higher deposit balance. At that instant, new money is created3.”

Now if you or I tried to create a deposit by writing numbers on our statement, we’d be arrested for fraud, but a banker doing the same thing is engaged in “money creation” and will likely receive a bonus. In addition to the reversal of causality compared to our fairytale version of reality we also need to accept that a large amount of lending does not go to fund Business Z which creates a step-up in economic activity (GDP) by expanding. In fact, I estimate that over 80% of new loans go to activities that either don’t directly grow GDP or at best increase it only marginally. The bulk of lending is going to mortgages, which tend to push up prices of existing housing stock, commercial real estate and consumer loans which bring forward some demand, which subsequently reverses as loans are repaid.

There is one more step that we need to get in order to understand the central banks’ role in new money creation. The central bank is de facto the bank for commercial banks who have deposits with the central bank. These deposits are just deposits, althought they are confusingly called “Bank Reserves” by bankers.

I’ll go through the details of how the BoE created £ 900 billion to buy bonds in Part 2 of this article, but in the meantime it is enough to say that the process was exactly the same as the generic example described above, the Bank of England firstly made a very large loan to the Asset Purchase Fund Facility Limited (APFF) in order to create a deposit.

The BoE lent these billions to the newly set-up company APFF with £ 100 in capital and no trading history (company 06806063. And, yes, I did notice).

So at the moment of lending, the BoE de facto created a deposit which allowed the Asset Purchase Fund Facility (APPF) to pay for the purchase of government bonds (gilts) from dealers, pension funds and insurance companies. Of course, these arrangements don’t make commercial sense, but that is because they are part of a confidence trick (con) that is required to keep people believing in the value of fiat currency.

In exchange, the APFF then transferred funds to the sellers of those gilts (dealers, pension funds etc.) which meant that those pension funds then had larger deposits in their own bank accounts. Eventually it meant that commercial banks ended up with larger deposits (confusingly also called reserves) with the Bank of England (I’ll cover this in Part 2, but right now, it is not important. I have also included a diagram below for subscribers).

At the same time the Treasury (the ministry of finance) was borrowing huge amounts of money by issuing vast amounts of new bonds (gilts). As we discussed in the last note peak bond issuance reached £ 62.5 billion in the month of March 2020 alone. In order to avoid appearing to be a banana republic, APFF cannot buy newly issued bonds directly from the government. Since we are a civilised advanced economy, the Bank of England (via the APFF) can only buy bonds that have been in circulation for one week4. So de facto the money that the APFF was using to buy from the dealers and pensions, was immediately being used by those same organisations to buy newly issued bonds from the Treasury. We know that from the stock of holdings where we can see that the monthly increase in the APFF’s holding of government bonds (gilts) was approximately equal to the size of the new bonds being issued by the Treasury. These arrangements are a ruse to channel freshly printed money from the Bank of England to the Treasury by using the private sector as an intermediary (more on this in Part 2).

The key thing to understand for now is that the Bank of England’s balance sheet grows significantly when it is creating money. On the asset side, the multi-billion pound loan to APFF shows up and on the liability side is the deposits of commercial banks which grow as the APFF transfers its money to the sellers of gilts (as an aside the fact that Bank of England shows this operation as a loan to APFF is ridiculous because it is “lending” to its own 100% owned subsidiary).

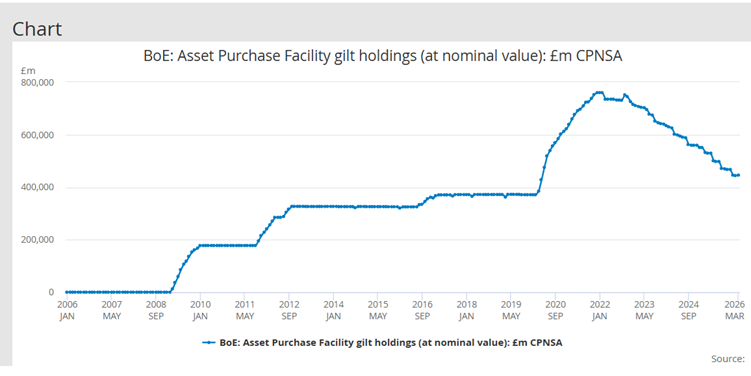

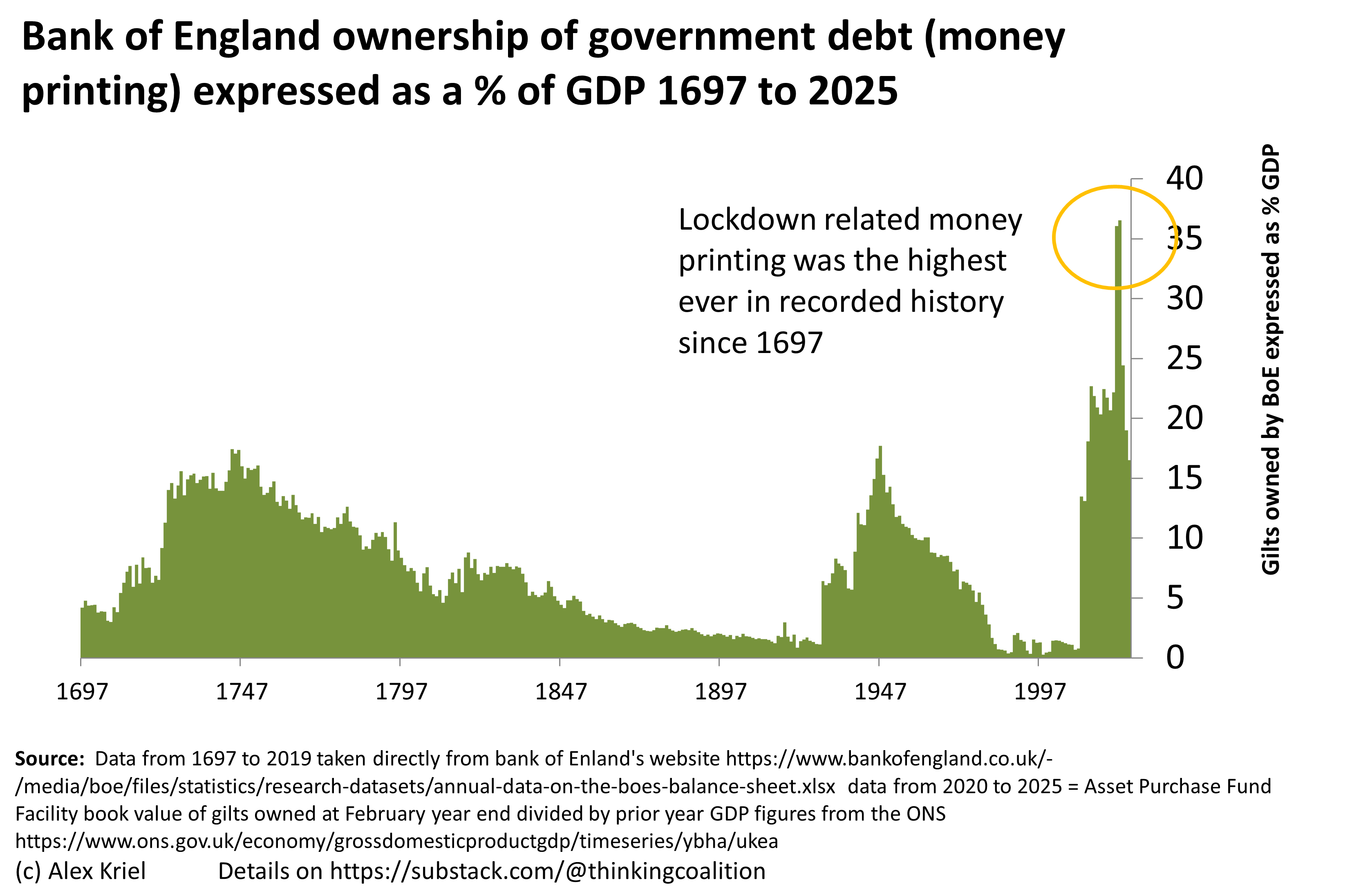

To be fair to the authorities, they did provide a lot of data about what is happening, but the dishonest mainstream propaganda media is not informing the public about this this topic. In reality the topic of the erosion of the buying power of people’s money was (and is) absolutely mission critical and should be at the heart of any and all reports about finance. Below is a time series for APFF’s ownership of UK government debt, in nominal (as opposed to market price) terms directly from the ONS5.

You can see how quickly the bureaucrats have become addicted to money creation as a “policy tool” (in truth a confidence trick which enriches vested interest and represents another step towards the economic cliff edge). The “emergency” intervention in 2009, spearheaded by big state socialist Gordon Brown, went on to grow for the next seventeen years and counting.

To give you some idea about the scale of this this money creation, £ 800 billion (at nominal values) is equivalent to the entire UK defence budget for 13 years. It is equal to 40% of the entire balance of household deposits and is around 38% of GDP (note these are only APFF’s government bond holdings, it also has some corporate bond holdings). This level of money printing took the bank of England’s ownership of government debt to 36.5 %, in 2022 the highest level in recorded history since 1697.

So the public who lock up their households at night to keep themselves and their property safe, who look over their shoulder before withdrawing money from an ATM lest it be stolen find that, invisibly and mysteriously, their money decreases in value. The public who don’t own property and who work to earn a wage to pay rent and buy food find that their earnings are worth progressively less and that while their income is “sticky,” their outgoings are not.

This debasement of money is one of the biggest burdens we face in our society. An enormous problem that any government worthy of the name would seek to fix it. And that’s why it comes as a shock that the invisible process is actually the intended result of the government’s policy!

As I mentioned in my last note, according to Ray Dalio the plan is to eventually default on government debt by inflating it away and that requires a high degree of stealth which I suspect is why nobody explains this stuff.

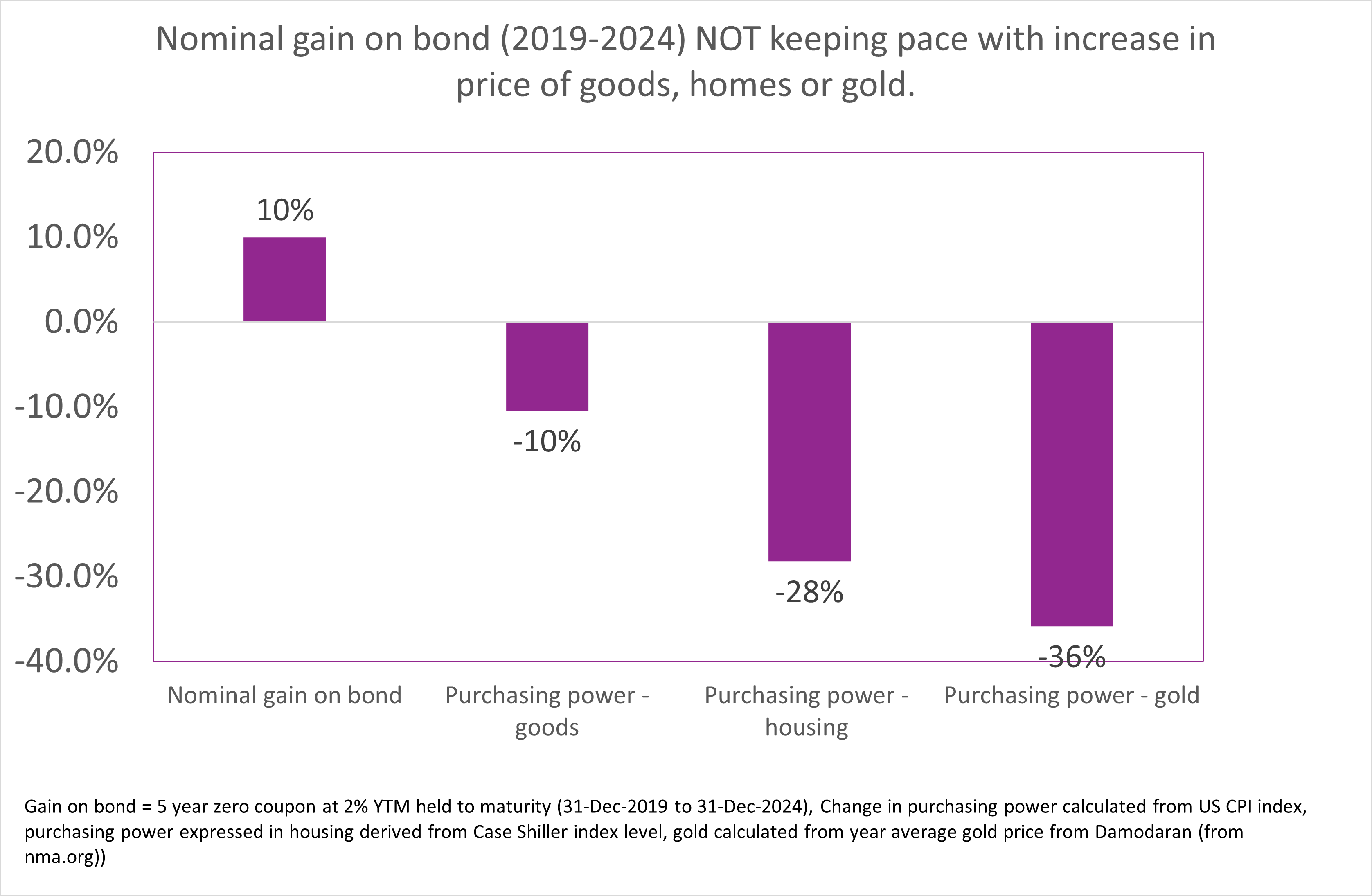

Some people instinctively understand the dangers of money creation and have sensibly been buying gold (a good idea up to a certain price). In fact, Western currencies have started to devalue against all other assets. I created the chart below for the US Dollar because the US has the most accessible data, but this picture will be repeated for most Western currencies with US Dollar with nominal interest interest is still falling against goods and services (inflation), houses (Case Shiller) and gold (ounces purchased).

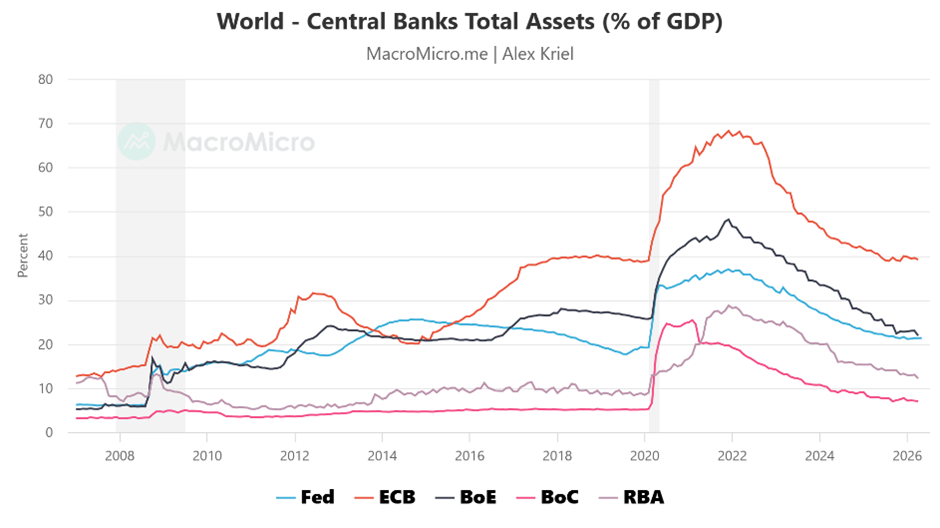

In fact, it is noticeable that pretty well all Western central banks started money creation (bond buying) at exactly the same time, they then increased this buying up to roughly comparable levels as a percentage of GDP and then reversed the process around the same time and at the same rate. You would have to be fairly naïve to imagine that this is all random and that “independent” countries all with “independent” central banks all separately decided to pursue exactly the same policy choices at exactly the same time. The fact is that there is a high degree of coordination in the actions of different Western central banks around the world.

(note that the above chart is total central banks assets, the APFF loan discussed above is around 75% of Bank of England assets which is why the Bank of England’s total assets peak at almost 50% of GDP in early 2022).

What does all of this mean for me?