The Great Debt Reset

As a follow-on from some of the economic data I looked at for David Fleming of Independent Alliance, I thought I would look at a related question, namely: Are we close to a financial meltdown? Although we haven’t seen a financial meltdown in a major Western economy for a long time, it is worth remembering that over the very long term, debt and currency crises are the rule, rather than the exception. I am again going to focus on the United States as an example, largely because they have excellent data on debt levels and very good graphing tools. The situation in the Euro Area and the United Kingdom are comparable to the United States.

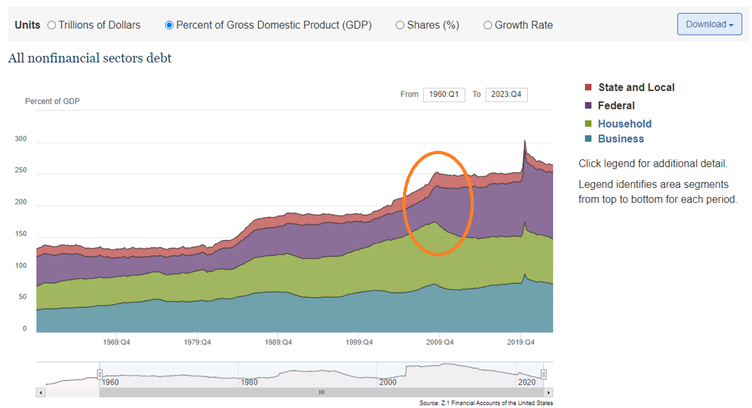

Debt levels are often considered in isolation, for example consumer debt, or government debt but ultimately they are all claims on various sectors within the economy. To talk sensibly about debt it is necessary to aggregate debt across the different borrowers in the economy and compare the total to the overall size of an economy. This is exactly what this chart from the Federal Reserve does by adding up four groups in the economy shown on the right of the chart and comparing the debts of each group to GDP to give the answer that total debt of these economic actors (borrowers) is 264% of GDP or 2.6x GDP1. That is down from a temporary peak of 300% at the start of lockdown, but that was something of a statistical quirk achieved in the second quarter of 2020. (The IMF’s equivalent numbers for the Euro Area and the U.K. were 254% and 252% respectively at the end of 20222).

Overall, you can see the long secular trend of increasingly leverage, but one thing that stands out for me is that the fact that the total debt picture is now meaningfully worse than it was in 2008 (233% in Q1:2008), when the consensus was that it was excessive leverage that caused the Great Financial Crisis of 2008-09. So today, the United States is 30% of GDP more indebted than it was in the overleveraged period of 2008. To be fair, the leverage of the household sector (green) has gone down when expressed as a percentage of GDP since early 2009, but you can see that this has been more than offset by the jaw-dropping increase in Federal Government debt (purple).

Federal debt on its own is around 100% of GDP which is the highest it has been since 1947 in the immediate aftermath of World War 2.

Deficits to infinity and beyond

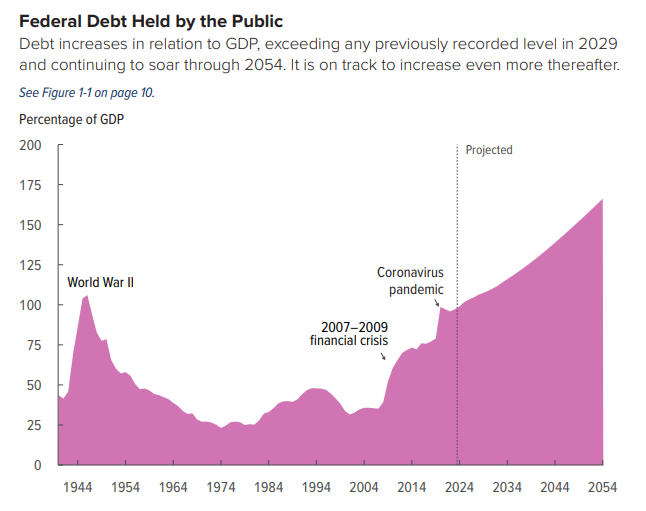

The U.S. Congressional Budget Office recently projected that Federal deficits will, in the words of Buzz Lightyear, continue to infinity and beyond! Their March 2024 report sets out that U.S. Federal debt will reach the highest level ever recorded by 2029 and that on this trajectory it will reach 166% of GDP by 20543. Of course, making projections until 2054 is fraught with danger, my guess is that this type of scenario will run into the reality that lenders will be increasingly unwilling to lend in the future.

If the other actors in the economy maintain their levels of leverage (households and business) then total debt will end up at 325% of GDP, or 3.25 times GDP.

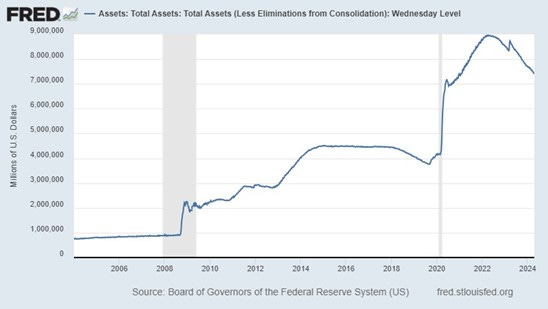

This type of situation is late stage empire collapse territory, especially in conjunction with very significant money printing, which I covered in the previous note. The chart below shows the Federal Reserve’s total balance sheet assets, which is a reasonable proxy for money printing. Although total assets have pulled back from USD 9 trillion, they are still very high at USD 7.5 trillion.

Reducing government debt burdens relative to GDP can be achieved by;

· Increasing taxes/reducing spending.

· Achieving real (inflation adjusted)growth.

· Devaluing the currency through money printing, thereby inflating nominal GDP.

· Default and restructuring.

Based on the Congressional Budget Office’s projections there doesn’t seem to be any interest in Washington in bringing the Federal budget into any kind of balance, let alone a primary (pre-interest) surplus. Based on the expansion of the Federal Reserve balance sheet, it appears that money printing has been chosen as the weapon of choice. As we discussed in the previous note, this will create a small number of winners (owners of certain financial assets) and a whole lot of losers.

Are we near a collapse?

Ray Dalio’s book The Changing World Order focuses a lot on economic and related factors that drive every empire’s boom and bust cycle, interestingly he does not appear to mention the role of religion. By contrast, Sir John Glubb’s paper, the Fate of Empires focuses on the importance of religion and ethics in driving the boom and bust cycles. However, both approaches appear to arrive at roughly the same conclusion that the lifespan of a typical empire is around 250 years, if the U.S. started around 1776, then we are in the final innings.

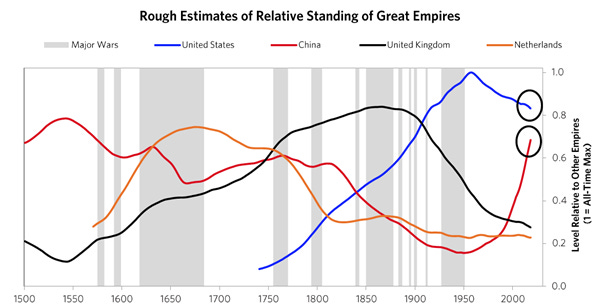

This chart below is from an article also by Ray Dalio4, which shows the relative standing of the Dutch, British and American empires over time, with one ascending at its predecessor declines. The line is a composite of 18 measures that he uses to quantify a country’s wealth and power. Dalio’s chart indicates that U.S. power peaked around 1950 and has declined since then. Based on recent trends, it appears that China will soon replace the United States as the world’s most powerful country. Doubtless this is driving the process of alliance formation with the collective West forming alliances against an increasingly cooperative China, Russia, Iran plus others grouping.

When will it happen?

The best that you can hope to achieve is to identify a general trajectory, the exact timing of when a dislocation in U.S. treasuries (for example) is impossible to know. Gold prices expressed in U.S. Dollars and (other currencies) are already showing a devaluation of the U.S. Dollar and other currencies. The other indicator to watch is the ongoing pull- back of foreign central bank holdings of U.S. treasuries, this indicator is moving sideways in an environment where the volume of treasuries is increasing enormously, due to the large Federal deficits discussed above. This implies that the share of foreign central bank holdings of treasuries is falling quite significantly. This is something that we can look at another time.

Leftists generally believe that Government deficits and resulting Government debt don’t matter and always revert to the example of Japan, where public debt stands at 261% to GDP to claim that there is nothing to worry about. There is no magic number where the wheels will suddenly come off and high debt levels can be fine until all of a sudden they are not fine, that is a question of confidence which can evaporate at any time. The U.S.’s high debt burden relative to historic levels, huge forecast deficits and large scale money printing all suggest a bust down the road. The only way to deal with this is to think about diversifying out of “safe haven” assets like treasuries and look at non-monetary assets (real estate, precious metals, art) and other hedges.

I hope to do one more article in this series which will look at the shifting of central bank assets.

Let me have you comments below.

Thanks

Alex

Alex Kriel is by training a physicist and was one of the first people to highlight the flawed nature of the Imperial COVID model5, he is a founder of the Thinking Coalition which comprises a group of citizens who are concerned about Government overreach (www.thinkingcoalition.com)

https://www.imf.org/-/media/Files/Conferences/2023/2023-09-2023-global-debt-monitor.ashx

https://www.linkedin.com/pulse/big-cycles-over-last-500-years-ray-dalio/

Thanks Alex. Very thought provoking and a subject I don’t know enough about, so thanks for sharing. Need to read it again and will look forward to the next one.

Good read with solid analysis. With the ongoing push of trans ideology and a persistent drive towards fascist / communist principles that appear deep-rooted within Govt's, Public bodies, institutions, quangos, media and education, one can't help but feel we are witnessing is a knee-jerk reaction within a governing elite to changing circumstances what will show their beliefs, principles and actions to be based on foundations built on nothing but quicksand. We are certainly in the decline of empires and nothing will change the direction of travel. About time too, I suspect.